All Industry Research

What Happens When Short Interest Exceeds 100 Percent

Published

February 18, 2022

Topic

Regulation and Reporting

Type

MFA Report

Share

Table of Contents

Key Points

- It is very rare for short interest in a company to reach the levels that GameStop experienced. In fact, there have only been 14 instances in the last 12 years that a U.S. company has experienced short interest exceeding 100 percent of its tradable shares.

- 8 of the 14 companies were very small and mostly controlled by company insiders, meaning that the available float was negligible, and this drove up the ratio of short interest to float.

- For the other 6 companies, heightened short selling did not lead to breakdowns in broader market functioning. The securities lending market has built in stabilizers – price and options to “fail” to deliver – that have permitted the market to function smoothly.

Report

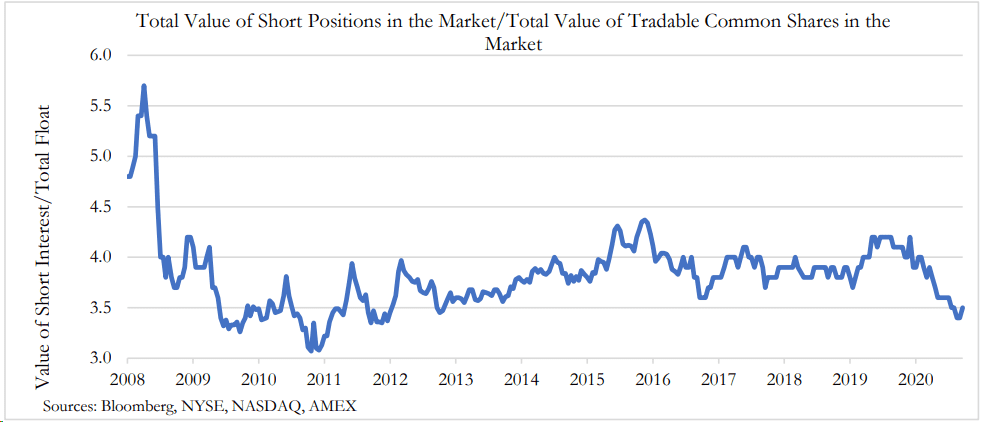

Short interest in a company represents the value of shares that market participants have borrowed to sell short in expectation that the price will decline. It is often expressed as a percent and is calculated by dividing the value of short sales for a particular security by the value of freely floating shares outstanding and tradable. Short interest can be referenced to understand how the market views a specific company, and when aggregated can shed some light on overall market sentiment. Aggregate short interest in the U.S. has been at low levels since the 2008/09 financial crisis. But a few individual companies – very few – have experienced high short interest. In this note, we examine all the cases since 2010 where short interest exceeded 100 percent, and we find that in all 14 instances, the dynamics were idiosyncratic and did not pose any risk to broader stability of the financial system.

Total Value of Short Positions in the Market/Total Value of Tradeable Common Shares in the Market

How Does Short Interest Exceed 100 percent and Why is it So Rare?

When an investment manager has identified a security that it wishes to sell short it will: (1) borrow the security, (2) sell the security at the prevailing market price, (3) purchase the security at a later date, and (4) return the borrowed security to the original owner. When the security is sold in that second step, there is nothing preventing the new owner of the stock from relending it. Thus, the same share can be borrowed and lent several times, and potentially enough times that short interest exceeds 100 percent.

When looking at the data from 2010 to 2021, short interest in a Russell 3000 stock has only risen above 100 percent 14 times, and there has never been an instance when more than two stocks’ short interest exceeded 100 percent at the same time. It is not surprising that the number of stocks to exceed 100 percent short interest is so low, as the structure of the securities lending market has safeguards to ensure smooth functioning. Broker dealers adjust the cost of borrowing securities to balance high demand for short selling, and they also factor in the risk of the transaction failing. These mechanisms ensure that the level of short positions for a particular security remains sustainable.

Changes in the Cost to Borrow

Banks and broker-dealers are the market-makers in the securities lending markets. Typically, the interest rate on borrowing and lending stocks is quite low, however if there is a particularly high demand to short, scarcity can develop, driving up the cost to borrow. When demand for a stock, such as GameStop, rises, a bank acting on behalf of a customer willing to lend the security will increase the price for lending it. In this situation, the market refers to the elevated price for borrowing as a “special,” meaning the cost of borrowing that stock is higher than the cost of borrowing other stocks that are not as much in demand. These forces of supply and demand help to set the price when matching borrowers and lenders.

Fails and Buy-Ins

If the broker is unable to locate the security for a transaction that has been executed, the short seller may be forced to repurchase the security to cover the short position. This is called a buy-in. In other cases, a party to a transaction may fail to deliver the security being shorted for a variety of reasons. Brokers consider the risk of buy-ins and fails when setting borrowing rates for securities.

What Happens When Short Interest Rises Above 100 percent?

While it is very uncommon for short interest in a stock to rise above 100 percent, it has happened 14 times over the last decade. In 8 of these 14 cases, short interest appeared high because the freely available portion of shares was very small given many of the shares were owned by company insiders who could not trade them. In other words, short interest as a percentage looked high because the denominator was solow and very small portions of shares outstanding were trading.

In just 6 cases since 2010 short interest has meaningfully risen above 100 percent. In 4 out of the 6 cases short interest was only above 100 percent for a month or less, while in the cases of Dillard’s and GameStop, short interest was elevated for extended periods of time. When looking closely at these cases, it is apparent that stocks with low market capitalization, low borrowing rates, and sufficient liquidity have the potential for short interest to rise above 100 percent, including for extended periods of time. However, in nearly all these cases the heightened short selling was sustainable and did not lead to breakdowns in market functioning.

1. Horizon Therapeutics PLC (HZNP)

In 2012, Horizon Pharma, now Horizon Therapeutics, was a specialty pharmaceutical company that was developing medicines to target arthritis, pain, and inflammatory diseases. At the beginning of March 2012 short interest in the company briefly spiked to 465 percent. During this period, about 37 percent of shares in Horizon were tradeable, meaning the stock was relatively liquid. In addition, Horizon’s market capitalization was only $67.4 million, an all-time low since the company went public. After this brief period in early March short interest quickly came down and was only 8 percent by the end of the month.

2. Skullcandy (SKUL)

Skullcandy is a company which markets headphones, earphones, hands-free devices, audio backpacks, MP3 players, and other products. In May 2012 short interest in Skullcandy briefly rose above 100 percent, peaking at 111 percent. During the month where short interest was at heightened levels about 37 percent of shares in Skullcandy were tradeable, and market capitalization ranged from $440.6 million to $358.6 million. This again shows Skullcandy stock was liquid and its market capitalization was relatively low (by comparison the average S&P 500 company’s market capitalization in 2012 was about $3 billion). Short interest did not remain elevated for long as it decreased to 84 percent by the beginning of June and declined to 41 percent by the end of 2012.

3. Power Solutions International Inc (PSIX)

Power Solutions International is a company which designs, engineers, and manufactures emissions-certified, alternative-fuel power systems. At the beginning of April 2017 short interest in Power Solutions International rose to 107 percent, during which time about 35 percent of its shares where tradeable and its market capitalization was relatively low at $109.8 million. Short interest in Power Solutions dropped to 73 percent by the end of April and declined to only 9 percent by June 2017.

4. Entercom Communications Corp. (ETM)

Entercom Communications is an audio and entertainment company. On November 1, 2017, the U.S. filed a complaint alleging that Entercom Communications Corp.’s proposed acquisition of CBS Radio, Inc. would violate Section 7 of the Clayton Act, which prohibits mergers and acquisitions where the effect “may be substantially to lessen competition, or to tend to create a monopoly.” To resolve the complaint, Entercom was required to divest certain broadcast television stations in Boston, San Francisco, and Sacramento. Directly after these events short interest in Entercom rose to 110 percent, during which time about 68 percent of its shares were tradeable. Short interest did not remain elevated for long and declined to only 7 percent by the end of November 2017.

5. Dillard's Inc (DDS)

Dillard’s is a fashion retailer and department store. In May 2020, shortly after the COVID-19 pandemic dramatically reduced shopping at retail and department stores, short interest in Dillard’s rose to 101 percent and remained above or close to 100 percent until December 2020. Throughout this period, between 27-39 percent of shares in Dillard’s were tradeable, meaning the stock was relatively liquid. Since late December 2020 short interest in Dillard’s has been declining and by February 2021 was only 32 percent.

6. GameStop Corp (GME)

Short interest in GameStop rose above 100 percent in December 2019, peaking at 149 percent in October 2020 (see chart below). During this time, market capitalization of GameStop dropped to $225.6 million, an all-time low since the company went public in 2009. Meanwhile, between 72-95 percent of shares in GameStop were tradeable, meaning the stock was extremely liquid. Since January 2021 short interest in GameStop has been declining and was only 33 percent in February 2021.

In Summary

Short interest rarely reaches levels above 100 percent because the securities lending market selfcorrects when short positions reach an unsustainable level as broker dealers adjust the cost of borrowing a security and account for the risk of buy-ins and fails. In the few cases when short interest has reached such heightened levels, it is because the characteristics of the security allowed high levels of short positions to be sustained without causing any disruptions to the market.

Related Research

October 14, 2020Commissioned Report

Economic contribution of the New Jersey securities, commodity contracts, and investments sector

September 1, 2019Commissioned Report

The Lifecycle of Data in Context: How Data Proliferation is Shaping Alternatives